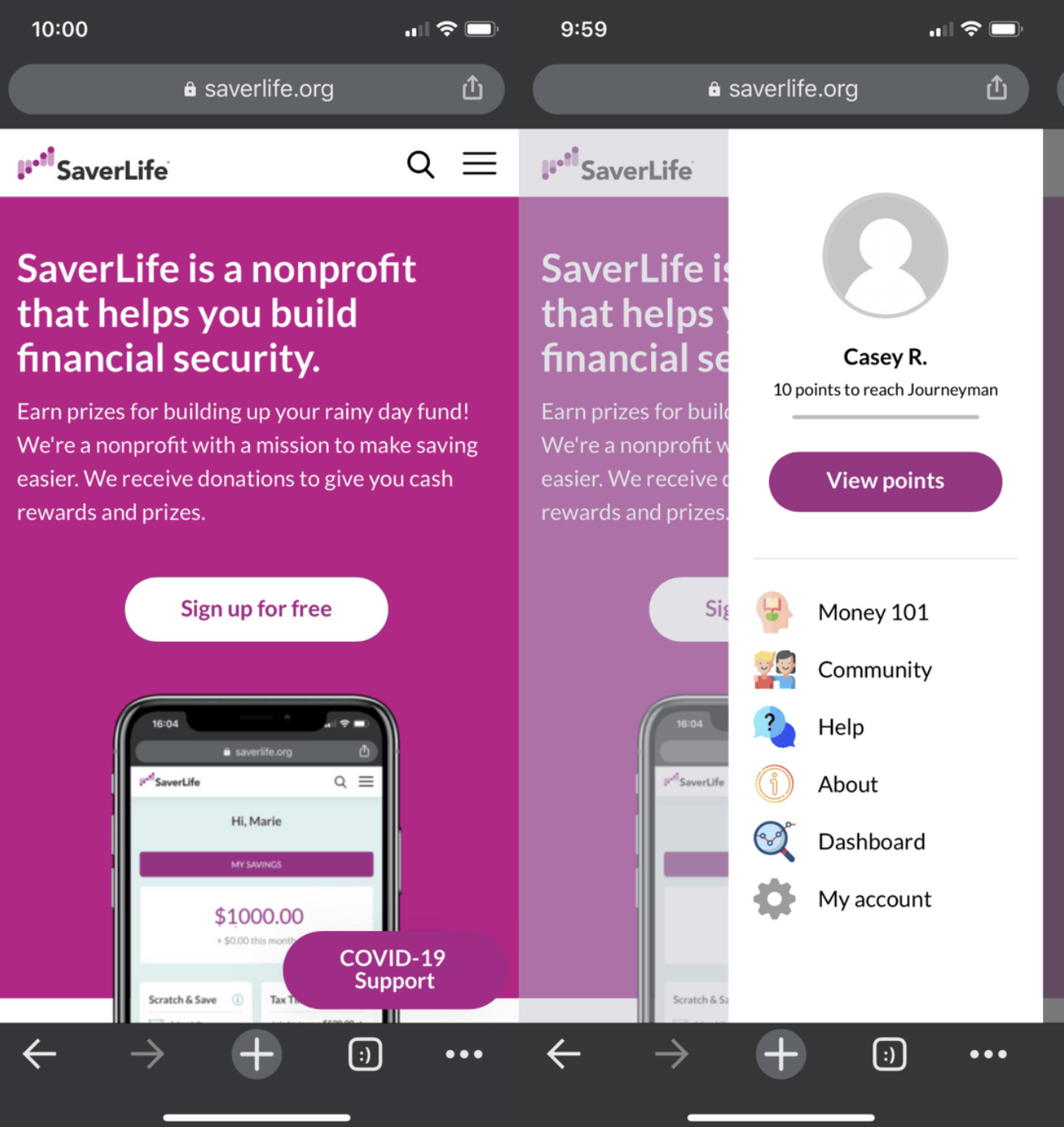

Before

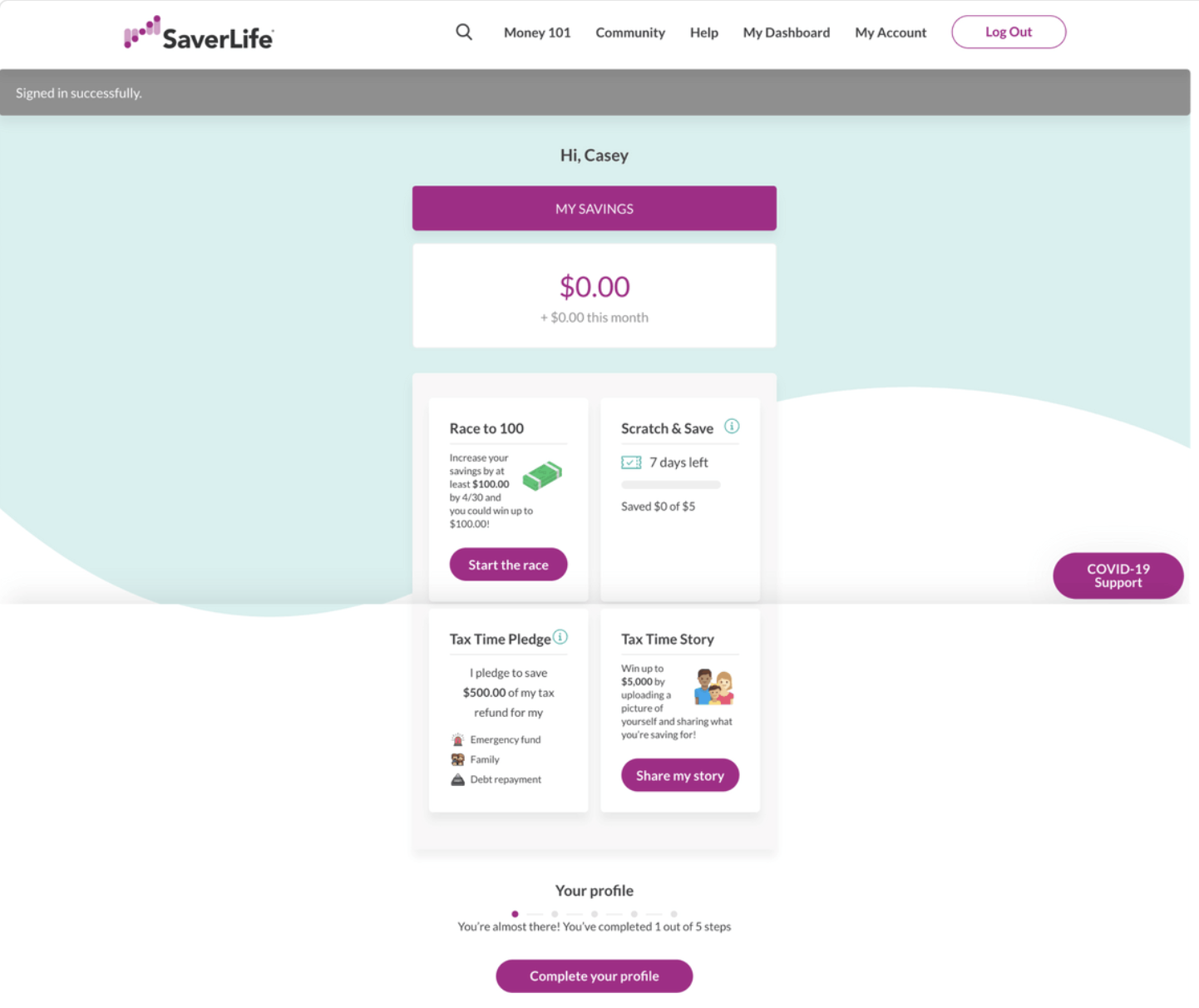

Scattered Features, No Habit Formed

What members experienced:

- Members saw SaverLife as a "lottery" not a savings tool

- Dashboard only showed sweepstakes challenges

- Majority of users never discovered the points system

- Gamification features hidden in hamburger menu

- No clear connection between actions and savings progress

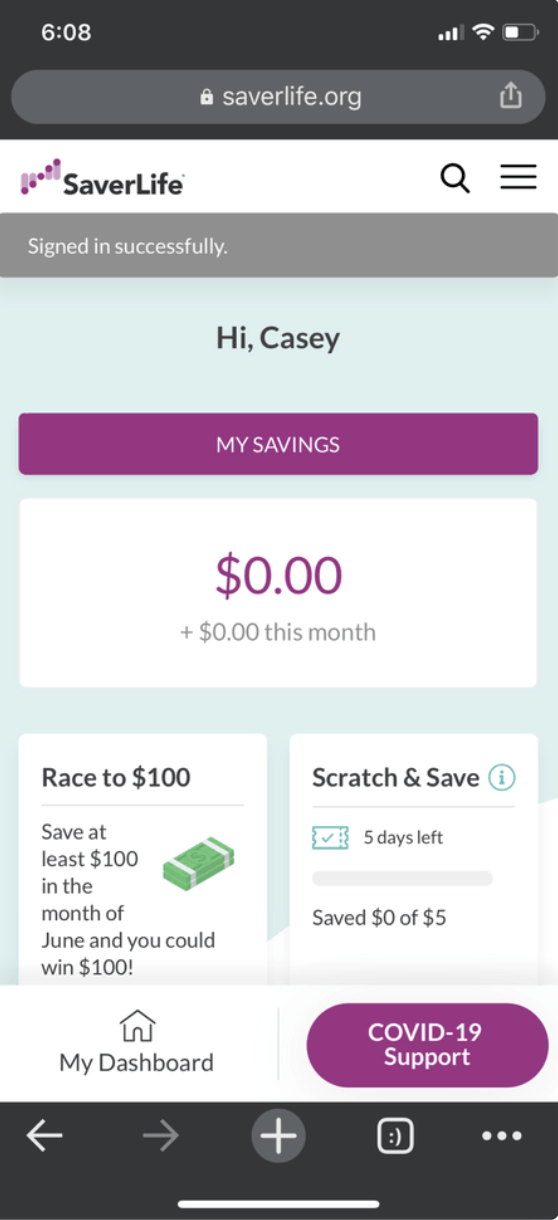

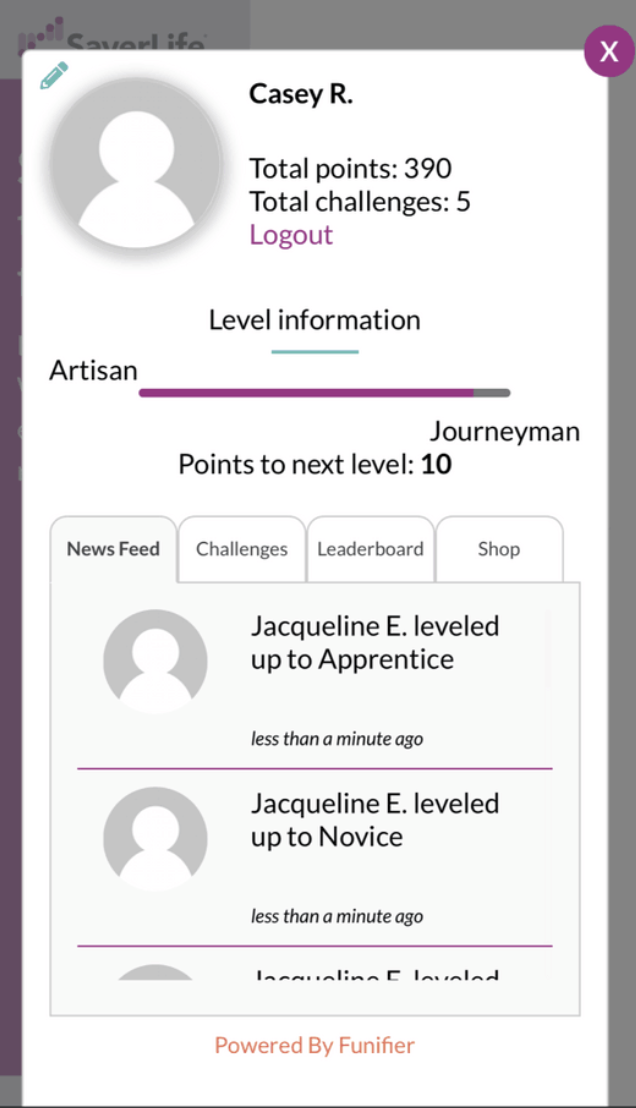

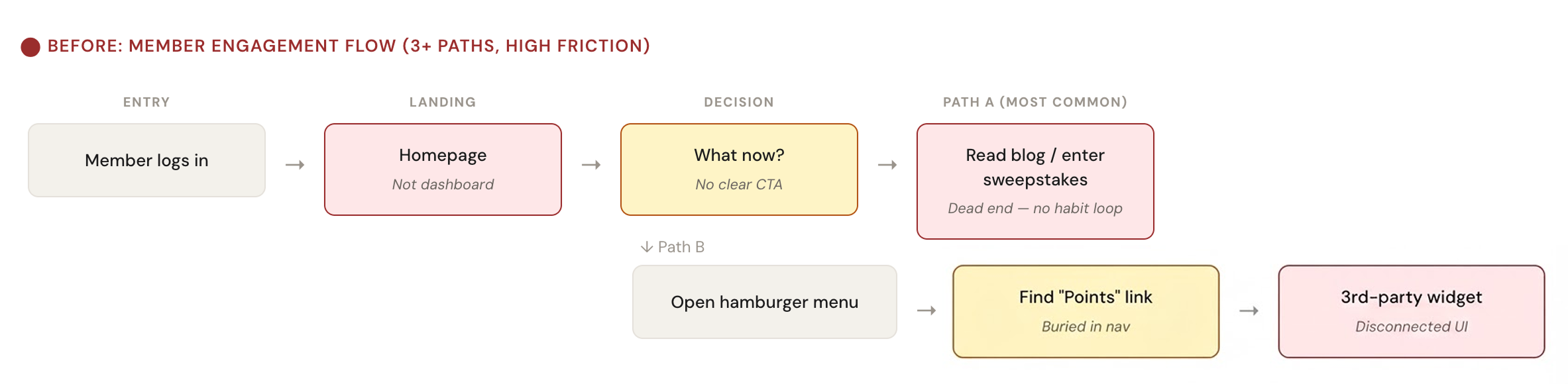

User flow

RETENTION PATTERN

Engagement spiked during sweepstakes promotions, but remained flat retention between events. This meant there was no habit formation loop.

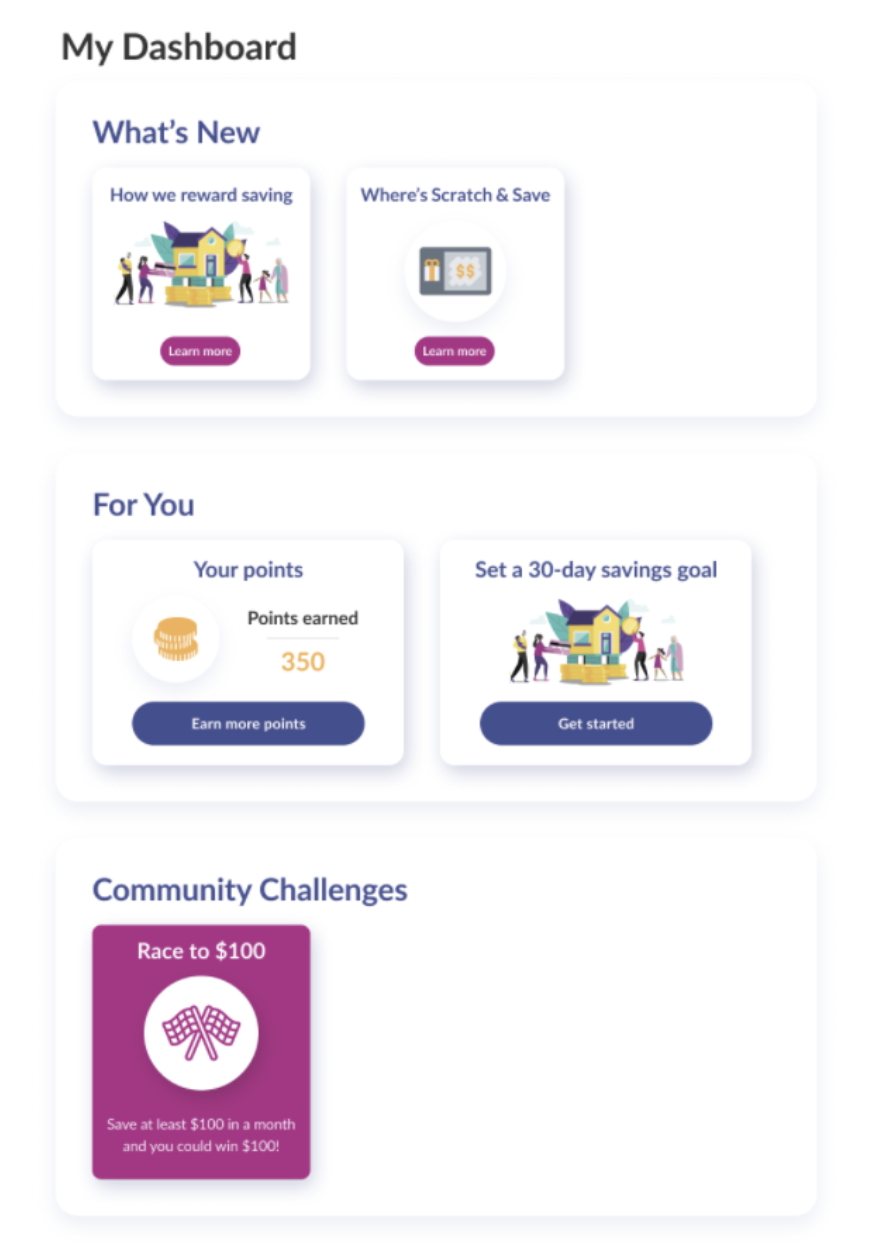

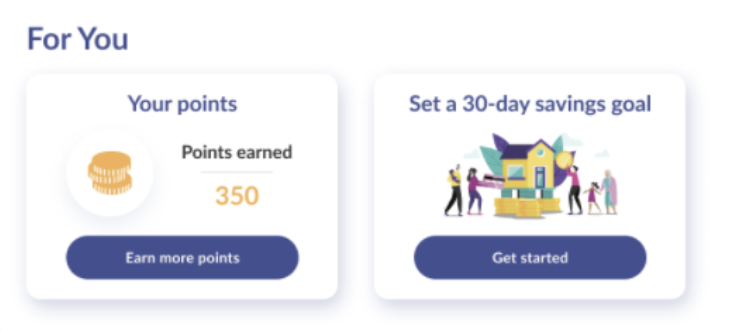

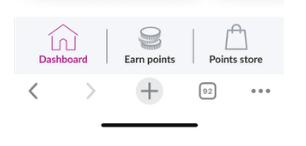

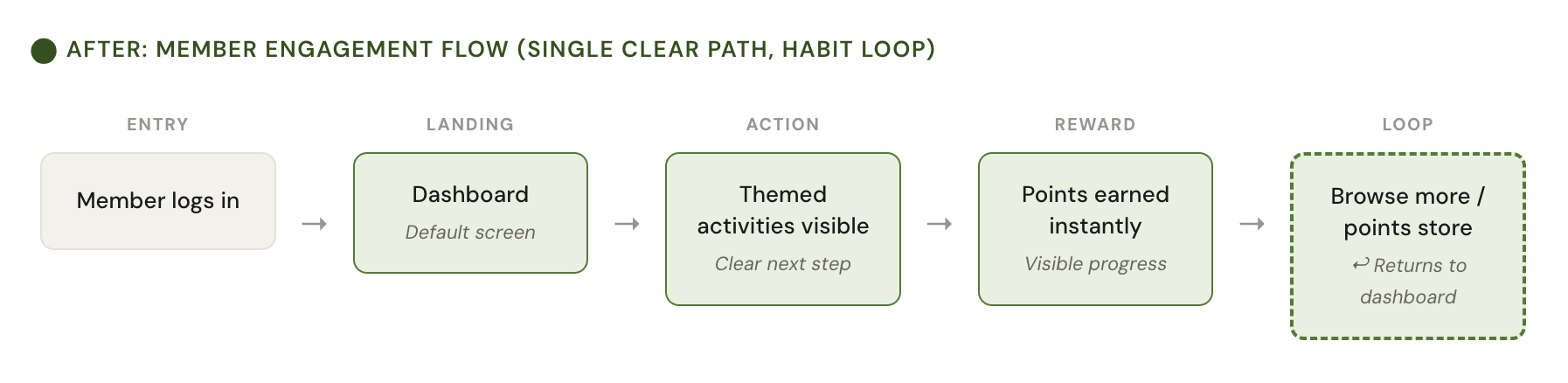

After

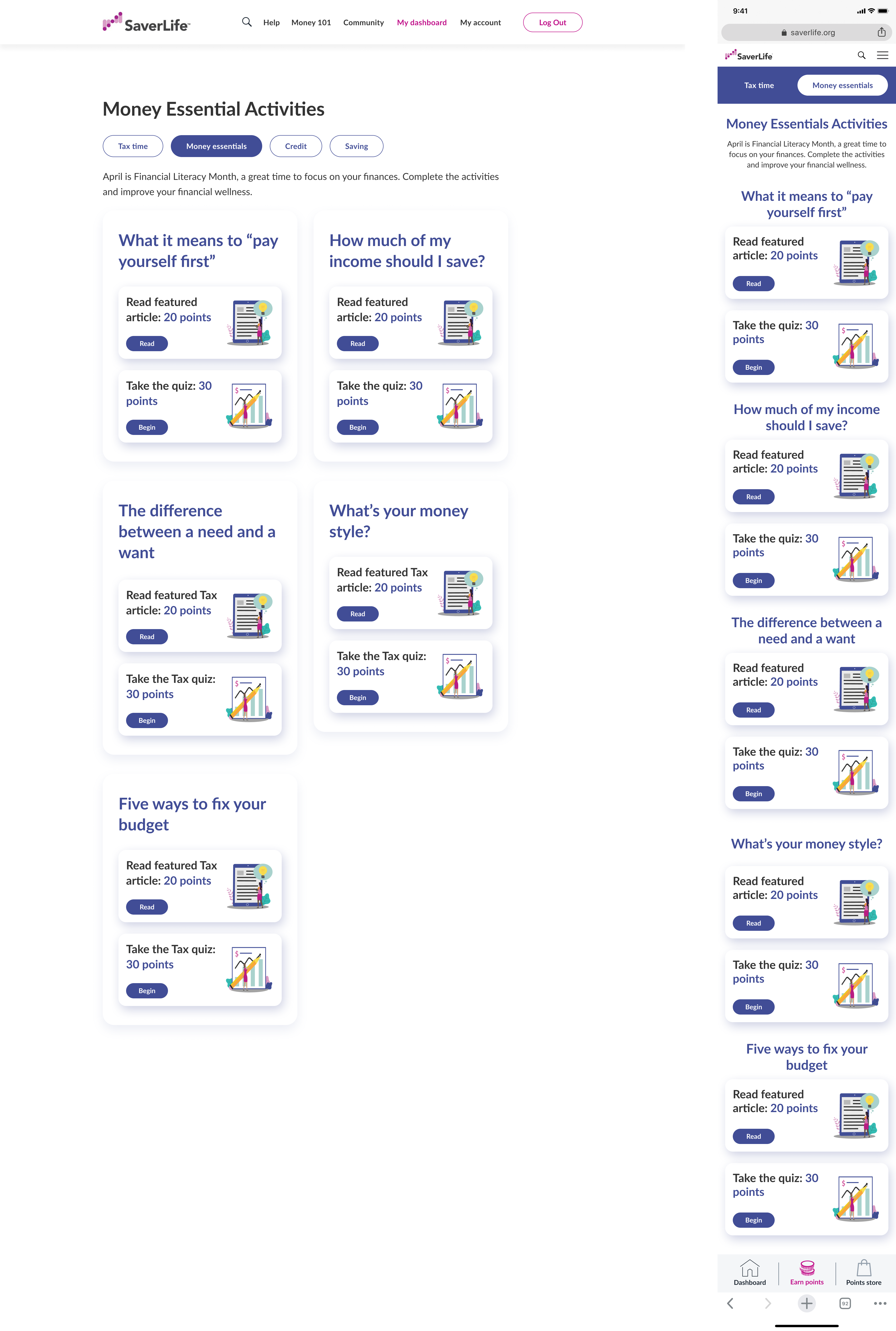

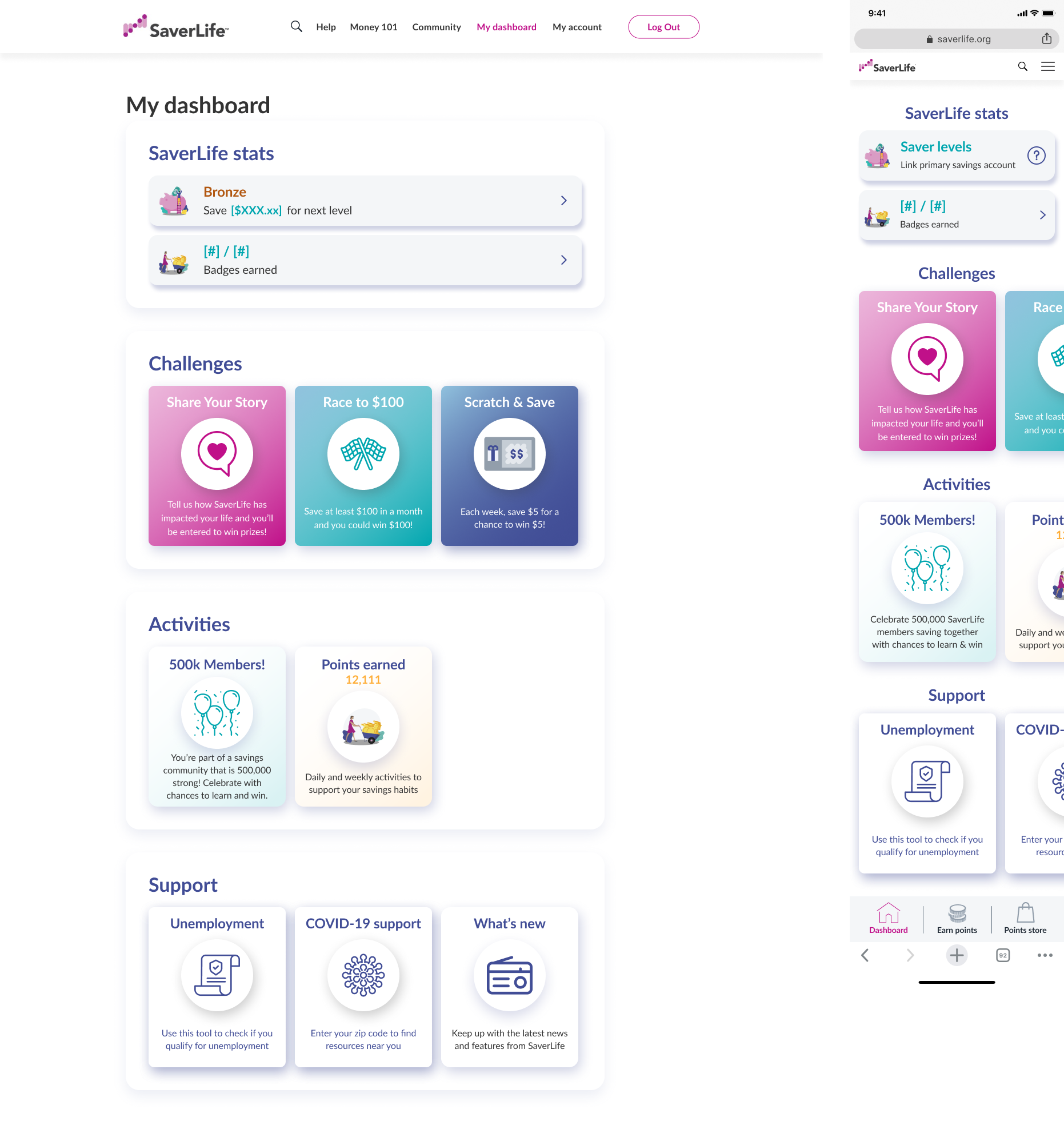

Cultivating a Desire to Save

What we changed:

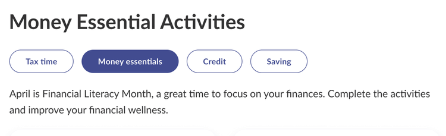

- Improved navigation and visuals of the dashboard

- Better highlighted core features

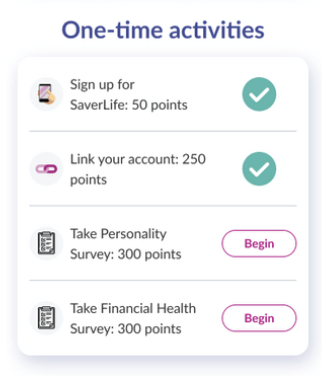

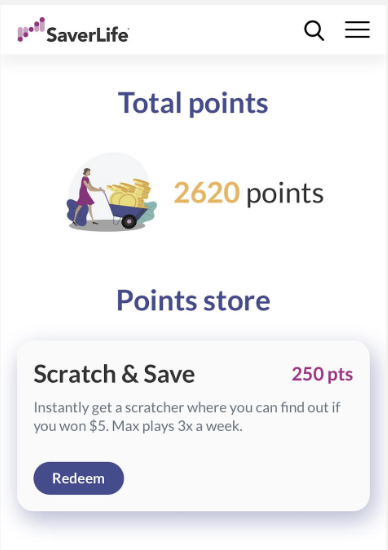

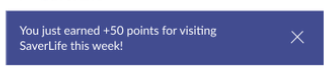

- Introduced points store and point activities

- Leveraged gamification to form habits = Created weekly engagement loops

User flow

KEY OUTCOME

2x Retention YOY and 2.5x weekly active users

This meant we established savings habits for a larger number of members than ever before.

This meant we established savings habits for a larger number of members than ever before.